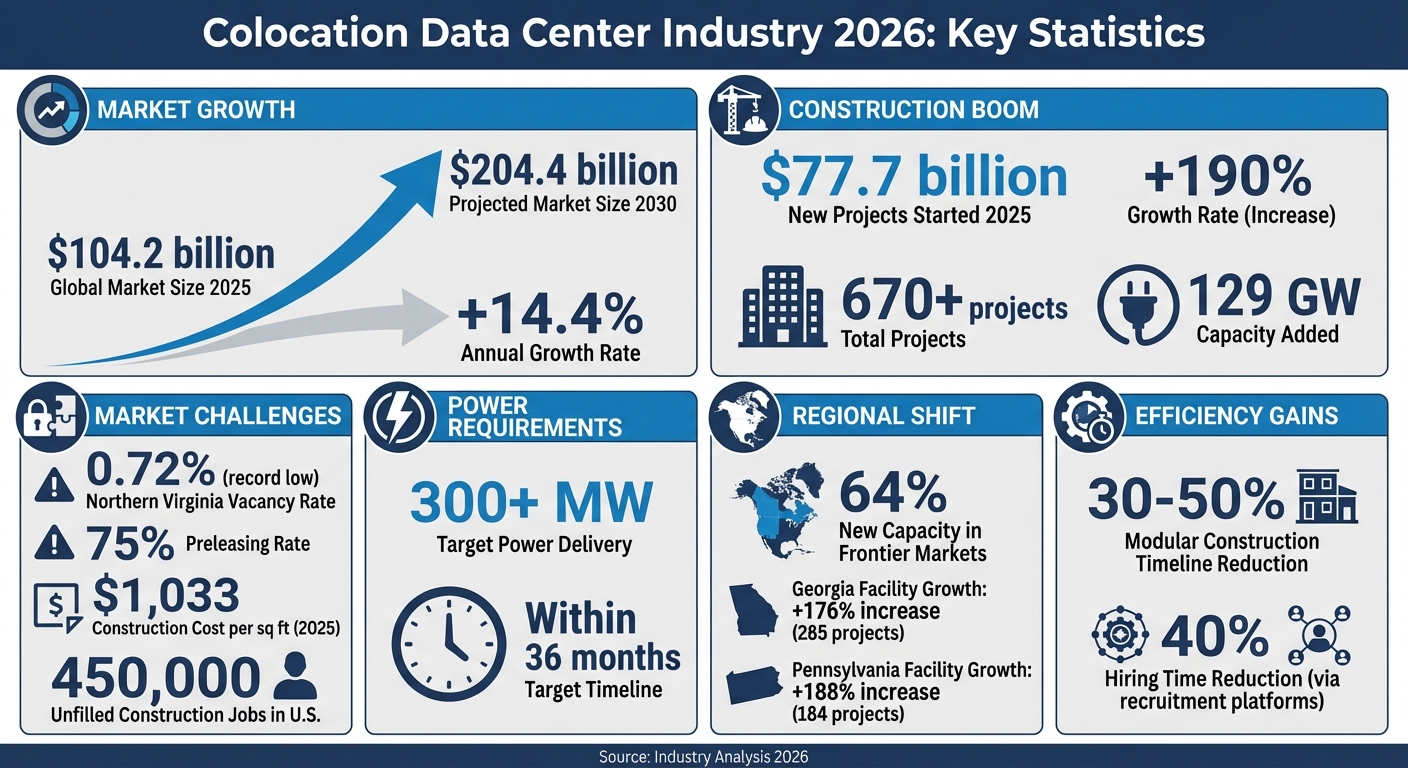

The colocation data center industry is experiencing rapid growth in 2026, driven by AI's demand for massive computing power. The global market is expected to double from $104.2 billion in 2025 to $204.4 billion by 2030, with a yearly growth rate of 14.4%. Key trends include:

Emerging markets like Ohio, Georgia, and Pennsylvania are drawing billions in investments due to faster grid access and lower costs. Developers are turning to modular construction, digital tools, and offsite fabrication to cut timelines by 30–50%. Recruiting platforms like iRecruit.co are addressing workforce gaps, reducing hiring times by 40%, and ensuring projects stay on track.

Demand is no longer the issue - the ability to deliver projects efficiently is now the industry’s biggest challenge.

Colocation Data Center Industry Growth Statistics 2025-2030

The colocation landscape is undergoing a major transformation in 2026. A striking 64% of new data center capacity under construction in North America is now in "frontier markets", moving away from traditional strongholds like Northern Virginia and Silicon Valley [5]. This marks a major shift in where and how the industry is choosing to grow.

The Midwest is stepping into the spotlight, with states like Ohio, Indiana, Wisconsin, Iowa, and Minnesota drawing billions in investments. Meanwhile, Georgia is on track for a 176% increase in data center facilities, with 285 projects either planned or underway. Similarly, Pennsylvania anticipates a 188% surge, with 184 facilities in the pipeline [7]. The Mountain West is also gaining momentum - Oregon, Utah, and cities such as Denver and Salt Lake City are each pulling in investments that exceed $1 billion [3][6].

Texas, while already a heavyweight, is expanding beyond Dallas into areas like West Texas, Houston, Austin, San Antonio, El Paso, and Abilene. Major projects include GridFree AI's South Dallas One facility, aiming for a 1.5 GW capacity, and OpenAI's Stargate initiative - a massive $100 billion project focused on advanced AI computing [1][6][5]. These developments are transforming previously untapped areas into thriving hubs that, in some cases, are surpassing the capacity of historic Tier 1 markets [5]. This growth isn’t just about funding - it’s also about the strategic advantages driving these shifts, which we’ll dive into next.

At the heart of this geographic shift is power availability. Primary markets face grid connection delays of over four years, while secondary markets offer quicker access to the electrical infrastructure essential for modern data center construction [5][1].

"Energy resources, not immediate proximity to an urban core, are now the primary site-selection driver." - Everett Thompson, CEO, Wired Real Estate Group [1]

Economic and regulatory perks are also playing a key role. Secondary markets offer lower costs for land, utilities, and construction. States like Pennsylvania and Indiana sweeten the deal with tax incentives and streamlined permitting processes [5][6]. Central Washington is becoming a hotspot too, thanks to its ability to support operations entirely with renewable hydroelectric power, aligning with sustainability objectives [6]. In Louisiana, the Meta Hyperion Campus is bypassing grid limitations entirely by using its own power generation resources [5].

"First and foremost, any regions that can deliver power to sites are going to have a leg up." - John McWilliams, Head of Data Center Insights, Cushman & Wakefield [6]

But this shift isn’t just about cutting costs - it’s also about speed to market. Secondary markets often offer faster permitting and entitlement processes, avoiding the delays and community pushback that are becoming more common in mature hubs [5]. These streamlined processes allow developers to bring facilities online months ahead of schedule, making these emerging markets an increasingly appealing choice for meeting urgent capacity needs.

The challenges of labor shortages are a pressing issue for the industry, especially as growth accelerates.

Modern colocation projects now demand enormous workforces. For instance, crew sizes on major campuses like DataBank's Red Oak campus have surged from 750 workers to as many as 4,000–5,000 by early 2026 [13]. Managing such a large number of workers requires careful planning and coordination.

Here’s how the workforce typically breaks down: about 40% of workers are in skilled trades, which translates to around 1,600 electricians and MEP specialists per site. Another 30% handle general labor, 20% focus on engineering and commissioning, and the remaining 10% are tasked with project oversight [4][10]. A good example of this scale is the Vantage Data Centers campus in Shackelford County, Texas. This $25 billion project spans 1,200 acres, boasts a 1.4 GW capacity, and is expected to generate 5,000 construction and operational jobs [12]. These roles often require expertise in cutting-edge technologies like liquid cooling and advanced power distribution systems, particularly for AI-driven designs [8][4].

Labor shortages are projected to hit their peak in late 2026 as the capacity built during 2024–2025 comes online [13]. By 2025, construction spending had already exceeded $52 billion, with over 60 projects - each valued at more than $50 billion - set to begin within six months [12]. Traditional project timelines of 12–18 months no longer hold; AI campuses now require multi-year schedules. Facilities with capacities exceeding 500 MW often need multiple substations and interconnections, which can extend construction timelines to 48 months or more [11].

Addressing these labor shortages requires forward-thinking strategies to secure skilled workers and streamline operations.

Engaging contractors early - 6 to 12 months before project start - has proven effective. This approach, combined with modular designs and digital tools, can cut timeline risks by 25% [4]. Hyperscalers also rely on long-term partnerships to reserve MEP specialists for AI-focused projects, helping to avoid delays of 20–30% and cost overruns of 15–25% [4].

Worker relocation programs are another solution, filling 30–40% of workforce gaps in secondary markets by offering incentives like housing stipends of up to $10,000 per worker [4][10]. These programs attract skilled labor to emerging hubs in the Midwest and Southeast, where land may be affordable but local talent is scarce. Additionally, modular construction and offsite fabrication methods are reducing the need for on-site labor [4].

Specialized recruitment platforms have also made hiring more efficient. By connecting projects to pre-vetted pools of workers, including hard-to-find commissioning agents, these platforms reduce hiring times by 50% and costs by 20% [9]. Developers are also turning to targeted recruitment campaigns, AI-driven matching tools, and internal training academies that combine classroom learning with hands-on fieldwork to meet the surging demand for skilled labor in AI infrastructure projects.

The cost to build colocation facilities has soared, climbing from $7.7 million to $10.7 million per megawatt (MW). This sharp increase is pressuring developers to manage costs while adhering to tight project timelines.

Several factors are driving these rising expenses. Copper prices, for instance, have surged by 36% year-over-year as of early 2026. At the same time, the growing demand for AI workloads has significantly increased rack densities - from 5–8 kW to as much as 15–50 kW per rack. This shift demands far more robust electrical and cooling systems, adding to overall infrastructure costs [14][15]. Compounding the issue, lead times for critical equipment have stretched to 12–18 months, requiring developers to commit capital earlier and absorb higher logistics costs [15].

Labor shortages are another major hurdle. With one-quarter of the construction workforce being foreign-born - half of whom are undocumented - strict immigration policies and aggressive deportation measures have driven up wages and project costs. Kenneth D. Simonson, Chief Economist at The Associated General Contractors of America, highlighted the issue:

"Aggressive deportations and immigration enforcement will hit construction much harder than they will most industries" [14]

High interest rates are further inflating financing costs for large-scale projects [14][16]. Delays in commissioning can be financially devastating. For example, postponing the launch of a typical 60 MW data center can cost developers around $14.2 million per month in lost revenue, labor overruns, and SLA penalties [15][17]. A six-month delay can slash a project's Internal Rate of Return (IRR) from 17.1% to just 8.8% [17]. With data center construction spending up 32% in 2025 and projected to grow another 26% in 2026 [16], keeping costs and schedules under control has become a top priority. To address these challenges, developers are turning to new, more efficient construction methods.

To combat rising costs and lengthy timelines, developers are adopting advanced construction methods that streamline processes and reduce expenses. Modular and prefabricated construction, for example, can cut project schedules by 30% to 50% compared to traditional approaches [15].

A standout example is GridFree AI’s South Dallas One project in Texas. Launched in December 2025, this site aims to deliver over 1.5 GW of capacity within just 24 months of lease signing by operating entirely off-grid, sidestepping traditional utility delays [1]. Modular container systems also play a key role, becoming operational in as little as 60–90 days - far quicker than the 18–24 months required for conventional builds [20]. Factory Acceptance Testing (FAT) at manufacturing sites helps identify potential issues before deployment, reducing risks and speeding up project completion [19][15].

Digital tools are further enhancing efficiency. By integrating design, fabrication, and installation into a unified digital system, often referred to as a Common Data Environment (CDE), developers gain real-time visibility into projects, minimizing costly rework [18]. BJ VanOrman, ERP Strategic Director at JE Dunn Construction, emphasized the benefits:

"Having all the information we need integrated within CMiC's single source of truth database... has provided our staff with the visibility they need to make better and quicker decisions" [15]

On-site precision has also improved with robotic total stations and laser scanners, ensuring that anchor bolts and embeds are installed with exceptional accuracy [18]. Meanwhile, AI-driven project management tools are expediting permitting processes and optimizing project controls [15].

Advanced cooling technologies are addressing the power demands of high-density racks. Liquid cooling systems, capable of supporting rack densities of 50–100 kW, can cut facility power consumption by 20% to 40% [15]. These innovations not only help manage escalating costs but also improve overall project execution. With skilled labor remaining scarce, the focus is shifting toward maximizing "execution capacity" - getting more done per labor hour - rather than simply increasing workforce numbers [2].

As workforce challenges evolve, securing specialized talent has become a critical component of successfully executing large-scale data center construction projects.

Recruiting the right talent for colocation data centers is becoming more difficult as demand skyrockets. The rapid growth of the market, especially for AI workloads, has created a pressing need for engineers with expertise in high-density rack deployments and advanced systems.

Currently, 5,242.5 MW of colocation capacity is under construction across the U.S., with 2,078.2 MW concentrated in Northern Virginia alone. This surge has stretched the talent pool to its limits [23]. Recruitment processes are often fragmented, with developers, hyperscalers, and colocation providers working in silos. This lack of coordination can lead to hiring delays, mismatched candidate qualifications, and extended timelines.

In secondary markets like Colorado, Indiana, and Pennsylvania, the pace of expansion has surpassed the capabilities of local talent pipelines. Meanwhile, primary markets face vacancy rates below 5%, and pre-leasing activity exceeds 70%, forcing providers to explore new regions where skilled labor is even scarcer [10][22].

Given these challenges, efficient recruitment strategies have become more important than ever.

iRecruit.co offers a tailored solution for addressing the unique hiring needs of mission-critical construction projects. The platform provides flexible recruitment plans, charging a 25% success fee on the first year's salary for single hires. For multiple positions, a monthly retainer starting at $4,000 per role (covering two positions) is available, with a reduced success fee of 20% [iRecruit.co pricing].

The platform’s pre-screening process combines AI-driven candidate matching, technical interviews, and reference checks to ensure that only highly qualified professionals move forward. This approach has resulted in a placement success rate exceeding 90% and a 40% reduction in time-to-hire [21][22].

With access to a database of over 50,000 vetted professionals, iRecruit.co is able to fast-track placements, often completing technical recruitment in under 30 days. This speed is critical as colocation providers prepare for nearly 100 GW of new capacity expected to come online between 2026 and 2030 [10]. By streamlining the hiring process, iRecruit.co helps ensure projects stay on schedule and within budget.

Executing colocation projects requires a wide range of specialized roles. Key positions include:

iRecruit.co excels at filling these critical roles by matching candidates to the specific demands of each project. For example, in Q1 2026, the platform successfully placed 15 MEP engineers for a colocation hub in Texas. This enabled the provider to stay on track with its ambitious timeline for a 200 MW campus. By focusing on candidates with experience in scalable, power-intensive environments, iRecruit.co helps colocation providers avoid delays and maintain efficiency [1][22].

By 2026, colocation data centers are focusing heavily on execution capacity through modular construction, standardized assemblies, and connected digital workflows [2].

"The biggest constraint in data center construction is execution capacity, not demand, capital, or land availability." - MSUITE [2]

Modular projects are now cutting schedules by 30% to 50%, with delivery timelines reduced to 16–20 months compared to the traditional 24–36 months [15]. However, equipment lead times for critical components like generators and switchgear still stretch between 12 and 18 months. This highlights the importance of integrated workflows that link design, fabrication, and field execution seamlessly. These advancements in efficiency also emphasize the need for a well-coordinated workforce strategy to match the pace of construction.

While modern construction methods address execution challenges, workforce planning is just as important. As project timelines shrink, the ability to recruit skilled professionals quickly becomes a critical factor in keeping projects on track. With rack densities rising sharply over the last five years, hiring the right MEP engineers, commissioning agents, and project managers is more crucial than ever [15].

Platforms like iRecruit.co are stepping in to solve this challenge. By reducing time-to-hire by 40% and achieving over 90% placement success rates, iRecruit.co ensures that projects stay on schedule and within budget. With access to a pool of over 50,000 vetted professionals and a hiring process that often completes in less than 30 days, the platform allows colocation providers to focus on execution without recruitment bottlenecks. As the industry shifts toward production-style construction and repeatable delivery models, efficient hiring strategies will remain a cornerstone of success.

Power is now the biggest hurdle for building new colocation facilities. The reasons? Grid limitations, the growing energy demands of AI workloads, and infrastructure issues. These challenges are slowing down power delivery, creating delays and bottlenecks. As a result, electricity availability has emerged as the main roadblock to scaling operations.

Secondary markets such as West Texas and Ohio are great options for quicker grid access. These regions offer plentiful resources, simplified permitting processes, and development driven by local resources. With over 64% of new capacity being developed in these growing markets, their role in expansion is becoming increasingly significant.

The toughest roles to fill in data center construction by 2026 are expected to include electricians, MEP engineers, commissioning specialists, and senior project managers. These positions are in short supply because the demand for skilled professionals continues to outpace the available workforce. Tackling these labor shortages will be essential to keeping up with the increasing demands of large-scale construction projects.